Get Money in Your Bank Account Today

- Quick bank loan offers & payments

- No paperwork, no guarantors

- Apply directly & safely online

Compare top lenders

Together with our partners, we provide access to up to 19 reputable banks and lenders. Explore offers tailored to your needs and choose the most suitable offer. Each lender abides by the regulations outlined by the South African National Credit Regulator (NCR).

What Are Bank Loans?

Bank loans refer to financial arrangements where banks provide funds to individuals or businesses to address specific financial requirements. These loans are typically structured with fixed repayment schedules, and interest is charged on the outstanding balance until full repayment is made.

When applying for a bank loan, borrowers are often required to pledge assets such as property or equipment as collateral. Should the borrower fail to meet repayment obligations, the lender has the legal right to seize and sell the pledged assets to recover the outstanding debt.

Types of Bank Loans

- Secured Bank Loan: Secured loans require borrowers to provide an asset, such as property or a vehicle, as collateral. For example, a mortgage loan involves the bank securing the financed property as collateral. If the borrower defaults, the bank can legally take possession of the property and sell it to cover the unpaid debt.

- Unsecured Bank Loan: Unsecured loans do not require any collateral. These loans are usually for smaller amounts and carry higher interest rates to offset the increased risk for the lender. Common examples include personal loans and credit card debt.

- Interbank Loan: In cases where commercial banks experience short-term liquidity shortages, they may borrow funds from other banks or directly from the Central Bank. These loans are typically short-term and are essential for maintaining daily operations or meeting reserve requirements.

Receive your loan offers immediately after filling up the loan application. Check what kind of loan offers you will get!

Components of a Loan

When taking out a loan, several critical factors influence its structure, the overall cost, and the timeline for repayment. Below is an overview of these components, explained in detail:

- Principal: This refers to the initial amount of money borrowed from the lender. It serves as the foundation upon which interest and other charges are calculated.

- Loan Term: The loan term indicates the total period within which the borrower must repay the loan. It can range from a few months to several years, depending on the loan agreement.

- Interest Rate: The interest rate represents the cost of borrowing and is typically expressed as an annual percentage rate (APR). It determines how much additional money the borrower will owe on top of the principal over time.

- Loan Payments: These are regular instalments—usually made monthly or weekly—required to meet the loan’s repayment conditions. The payment amount is influenced by the principal, the loan term, and the interest rate. Amortisation tables are often used to calculate these instalments.

Beyond these basic components, lenders may impose extra charges, such as origination fees, servicing fees, or penalties for late payments. For substantial loans, collateral may also be required. Collateral refers to valuable assets such as property or a vehicle that secure the loan. In cases of default, the lender has the right to seize the collateral to recover the unpaid debt.

No hidden fees, free application – no commitment

How Do Bank Loans Work?

Applying for a bank loan typically involves submitting an application form along with supporting documents, such as your company’s certificate of incorporation and financial statements.

Once all necessary documents are collected, the bank conducts a credit analysis of your business. This evaluation considers several factors, including your financial statements, cash flow, business plan, and asset coverage ratio, to determine if the loan should be approved.

If your application is successful, the bank will provide funds, which must be repaid with interest according to agreed terms.

In most cases, tangible assets must be offered as collateral. If the loan defaults, these assets may be seized and sold by the bank to recover the owed amount.

Banks have long been a primary source of funding for traditional businesses. However, they may not always be the best option for newer, fast-growing e-commerce businesses. These companies often lack sufficient assets to pledge and typically present higher risk-return profiles.

Who Can Apply for a Loan?

- You are over 18 years old

- You are employed and employment has lasted for more than 6 months

- Your loan should not be more than 8 times larger than your monthly income

Compare Loans Online in 3 Easy Steps

FILL IN OUR APPLICATION

Complete our loan application in minutes. Just enter your details and choose your desired loan amount.

CHOOSE A LOAN OFFER

Based on your responses, you will receive a variety of personalised offers from up to 19 lenders.

GET YOUR MONEY

You are free to accept or decline the offers as you please. The offers are non-binding.

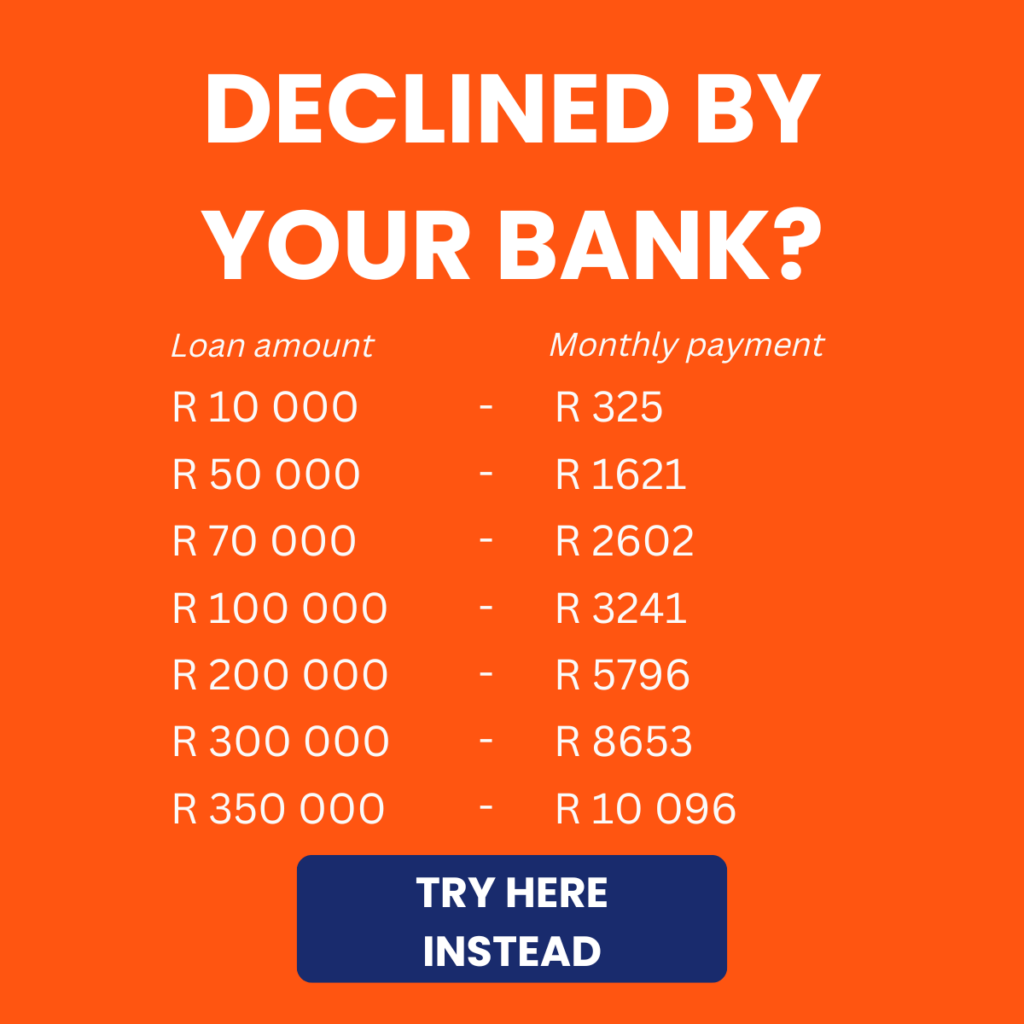

Flexible repayment from 6 to 72 months. Maximum APR 28%, as regulated by the NCR. Lender fees (initiation and monthly service) may apply. Checking your options with Arcadia Finance is free and won’t impact your credit score.

Loan Offerings from Various South African Lenders

| Lender | Loan Amount Range | Interest Rate (APR) | Loan Term |

|---|---|---|---|

| Capitec Bank | R10,000 – R500,000 | 13.5% – 29.25% | 1 – 7 years |

| First National Bank (FNB) | R1,000 – R360,000 | 17.5% – 29% | 1 – 6 years |

| DirectAxis | R5,000 – R300,000 | 24.5% – 28.25% | 2 – 6 years |

| African Bank | R2,000 – R250,000 | 15% – 24.5% | 7 months – 6 years |

| Absa | R3,000 – R350,000 | 13.75% – 29.25% | 1 – 7 years |

| Standard Bank | R3,000 – R300,000 | 10.5% – 27.5% | 1 – 7 years |

| Sanlam | R5,000 – R350,000 | 16% – 29% | 1 – 7 years |

Why Use Arcadia Finance?

- 100% free: The application is free and does not include any hidden fees.

- Quick & easy: The whole application process is done online in minutes.

- Convenient: Compare up to 19 banks & lenders with one application.

- Non-binding: You decide if you want to accept or decline your offers.

- Safe: Your personal data is safe with us.

What is Arcadia Finance?

Arcadia Finance helps South Africans in the search for loans from different banks and lenders through our loan broker partners. We provide access to up to 19 reputable banks and lenders. By completing our loan application you will get multiple loan offers, which you can compare and select the most suitable offer. The service we offer is completely free of charge and you will not commit to anything by requesting loan offers via Arcadia Finance. We only work with trusted loan brokers who collaborate with NCR licensed banks and lenders in South Africa.

Tips on Obtaining a Loan

To qualify for a loan, applicants must demonstrate both the ability and the financial discipline required to repay the borrowed amount. Lenders evaluate several key factors before deciding whether a borrower presents an acceptable level of risk. These factors include:

Income

For substantial loans, such as home mortgages, lenders often require borrowers to meet a minimum income threshold. This ensures the borrower has sufficient financial capacity to meet repayment obligations. Additionally, lenders may expect proof of stable employment over several years as an indicator of financial reliability.

Credit Score

A credit score reflects an individual’s creditworthiness, derived from their history of borrowing and repayment. Negative financial events, such as missed payments or bankruptcies, can significantly harm a credit score and reduce the likelihood of loan approval.

Debt-to-Income Ratio

Beyond income levels, lenders assess the borrower’s existing financial commitments by examining their credit history. The ratio of current debts to income helps lenders determine if the borrower is overextended. A high ratio suggests potential difficulty in managing additional debt repayments.

To improve the likelihood of securing a loan, it is essential to demonstrate responsible debt management. Pay off existing loans and credit card balances on time and avoid accruing unnecessary debt. Such financial habits not only improve eligibility but may also help secure more favourable interest rates.

Check your eligibility for FREE!

Pros and Cons of Bank Loans

Pros

- Defined Loan Terms: Bank loans provide fixed interest rates and repayment amounts from the beginning, ensuring clarity in financial planning and facilitating accurate budgeting.

- Ownership Retention: Borrowing from a bank does not require giving up any share in the ownership of your business.

- Comparatively Low Interest Rates: Bank loans typically offer interest rates that are lower than those associated with alternative financing methods such as invoice or inventory financing.

Cons

- Complex Application Process: Applying for a bank loan often involves gathering and submitting extensive documentation. This process can be both tedious and time-intensive.

- Collateral Requirements: Banks generally require collateral to secure the loan. E-commerce businesses, which may lack substantial tangible assets, could face difficulties meeting this condition. In such cases, personal assets may be required as security.

- Strict Eligibility Criteria: Many banks impose stringent requirements for loan eligibility, such as mandating that a business must have been operational for a specific number of years (e.g., two years or longer). Meeting creditworthiness standards can also be challenging.

Revenue-Based Financing as a Viable Alternative

Revenue-based financing (RBF) has emerged as an increasingly preferred funding option for small and medium-sized enterprises, startups, and e-commerce businesses in recent years.

This method provides an alternative to traditional bank loans by offering funding that is directly tied to a company’s future revenue performance.

Once an application for revenue-based financing is submitted, a thorough risk assessment of the business is conducted. If the application is successful, funds can typically be disbursed within 48 hours.

Unlike conventional bank loans, which require fixed repayment amounts at regular intervals, revenue-based financing offers flexibility. Repayments are adjusted according to the business’s monthly revenue, allowing for more manageable financial commitments during slower periods.

With the RBF model, funding platforms claim a small percentage of the business’s monthly revenue as repayment for the capital provided. If revenue is lower in a particular month, the repayment decreases accordingly. Conversely, during more profitable months, repayments are proportionately higher.

The total repayment amount is capped at a predetermined figure, often calculated as the capital provided plus a flat fee.

19

Banks & Brokers

Comparing

85%

South Africans

Approved for Loans

1 500 000

Users Compared Loans Through Arcadia

Should You Opt For Bank Loans Or Revenue-Based Financing?

Every business has distinct financial needs, making a one-size-fits-all approach to funding impractical. Long-term loans might appeal to some businesses due to their structured repayment schedules and predictability. In contrast, other businesses may benefit from the flexibility offered by RBF, particularly if their revenue streams are variable.

Each financing option comes with its own set of advantages and disadvantages. Business owners and decision-makers must carefully evaluate their unique circumstances and goals before determining the most appropriate option.

There is no universally superior financing solution. The best choice is the one that aligns with your business’s specific requirements and financial situation.

Secure your loan effortlessly with Arcadia Finance

The loan application is free, and you can pick from a variety of 19 respected lenders. We only work with trusted loan brokers who collaborate with NCR licensed banks and lenders in South Africa.

After submitting your loan application to us, we will send it through our loan broker partners to a number of different banks and lenders for review. Within minutes, you’ll receive a variety of loan options that are available for you. Select the one that best fits your needs.

Remember, all offers are no-binding, so if you don’t find what you’re looking for, you’re free to decline.

Conclusion

Bank loans remain a vital financing option for individuals and businesses in South Africa, offering structured terms, competitive interest rates, and clarity in repayment. While they are well-suited for traditional businesses with stable income and collateral, the stringent eligibility requirements and lengthy approval processes may limit accessibility for some. For businesses with fluctuating revenues or fewer assets, alternatives such as revenue-based financing may provide a more adaptable solution. Ultimately, choosing the right funding option depends on a thorough assessment of your business’s financial needs, risk profile, and long-term goals.

Frequently Asked Questions

Interest rates for bank loans in South Africa generally range from 10.5% to 29.25%, depending on factors such as the lender, loan type, and borrower’s credit profile.

Not all bank loans require collateral. Secured loans, such as mortgages, need collateral, while unsecured loans, like personal loans, do not. However, unsecured loans usually have higher interest rates.

The approval process for a bank loan can take several weeks to months, depending on the lender and the complexity of the application. Providing accurate and complete documentation can help speed up the process.

It depends on the type of loan. Some loans, like personal loans, offer flexibility in usage, while others, such as home loans or business loans, may have restrictions tied to specific purposes.

If your bank loan application is rejected, you can consider alternatives like revenue-based financing, peer-to-peer lending, or revisiting your application to address the issues highlighted by the lender, such as improving your credit score or providing additional collateral.