For many years, belonging to the middle class in South Africa was widely regarded as occupying a kind of financial safe zone – a position where having a steady job meant you could comfortably afford decent middle-income housing, perhaps drive a financed vehicle, and occasionally take the family away on holiday without too much worry.

Key Takeaways

- The COVID-19 pandemic dealt a lasting blow to middle-class finances: The ripple effects continue to reshape household budgets in ways many consumers are still struggling to fully come to terms with.

- The middle class punches above its weight in debt: Comprising only 10% to 15% of the population, this group carries a disproportionately large share of South Africa’s total consumer credit debt.

- Even comfortable earners are not immune: Those bringing home as much as R50 000 a month are feeling the squeeze, with many directing nearly three-quarters of their take-home pay toward debt repayments alone.

About Arcadia Finance

Arcadia Finance takes the stress out of securing a loan by offering a simple, fee-free application process and a selection of 19 reputable lenders, all fully registered with South Africa’s National Credit Regulator.

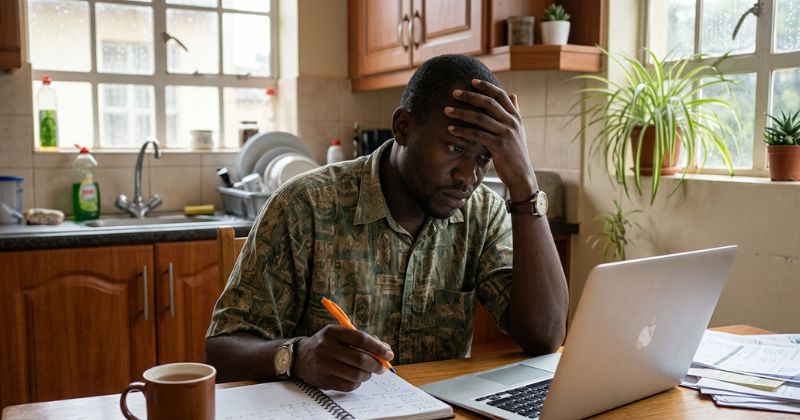

South Africa’s Middle Class Is Shrinking – and Drowning in Debt

However, that once-reassuring picture has changed dramatically and in many ways irrevocably, particularly in the wake of the devastating financial and psychological impact of the COVID-19 pandemic, according to debt counselling company National Debt Advisors (NDA). The ripple effects of that period continue to be felt across household budgets in ways that many consumers have yet to fully reckon with.

South Africa’s middle class is estimated to comprise between 10% and 15% of the population, depending on the income threshold used – yet this group carries a disproportionately large share of the country’s consumer credit debt.

Even R50 000-a-Month Earners Are Feeling the Pressure

Even people operating at the upper level of the middle class – those earning in the region of R50,000 per month – are feeling the financial squeeze right now, according to NDA’s Samantha Moyana. This is a figure that many South Africans would consider a comfortable income, yet even at this level, the pressure is becoming increasingly difficult to manage.

Moyana explains that consumers in this particular earning bracket typically direct roughly 74% of their take-home pay towards servicing debt obligations such as credit cards, vehicle finance arrangements and personal loans – leaving remarkably little room for anything else.

Financial advisors generally recommend that total debt repayments should not exceed 35% to 40% of take-home pay. At 74%, earners in this bracket are spending nearly double the recommended threshold on debt alone.

Why Higher Earnings Don’t Always Mean Greater Financial Security

This troubling pattern can be attributed to two compounding forces: the relentlessly increasing cost of living on one hand, and the tendency to borrow too much money on the other. Moyana notes that a higher income level also unlocks access to significantly more credit, which creates a particularly dangerous cycle.

She points out that as affordability increases on paper, so too does the credit that financial institutions are willing to extend – and many middle-class earners take full advantage of this access without adequately accounting for the cumulative weight of those repayments. These rising costs squeeze the middle class from both sides, and debt ultimately ends up filling the gap where savings should be.

As a practical illustration, consider a typical scenario described by NDA: a professional receives a fixed monthly salary, from which they commit to a home loan, finance a vehicle they need for daily commuting, pay tuition fees at a private school for their children, and cover a range of other standing monthly expenses. Each of those line items may seem individually justifiable – but together, they leave very little breathing room when any unexpected expense arrives.

How Earning More Can Lead to Owing More

A significant part of the problem, as NDA highlights, is the phenomenon known as lifestyle creep – a gradual but persistent pattern in which spending rises in step with income increases. As earnings go up, so do the associated expenses: a larger home in a better suburb, a second car for the household, a move to a more prestigious school for the children, more frequent dining out, and upgraded subscriptions and services across the board.

One effective way to guard against lifestyle creep is to automate a savings contribution every time you receive a salary increase – directing at least 50% of any raise straight into a savings or investment account before adjusting your lifestyle to match the new income level.

The insidious nature of lifestyle creep is that each individual upgrade feels entirely reasonable and well-deserved at the time. It is only when the full picture is viewed together – all the debit orders, all the monthly commitments, all the credit agreements – that the cumulative strain becomes clear.

Practical Steps to Protect Your Middle-Income Household

NDA outlines several concrete actions that middle-class earners can take to regain control of their finances before the situation becomes unmanageable. These are not theoretical suggestions – they are steps that debt counsellors work through with real clients on a regular basis.

Get Honest About Your Numbers

The starting point is a thorough and unflinching review of one’s full financial picture – listing every source of middle-class income, whether that is a salary, commission, freelance work or side income, alongside every single monthly debit order and repayment commitment. If the numbers do not make sense when written down clearly on paper, they will not magically resolve themselves in real life.

Use a spreadsheet or a budgeting app such as 22seven (which links directly to South African bank accounts) to get a real-time, consolidated view of where your money is going each month. Many people are genuinely surprised by what they discover.

Cut Lifestyle Costs Before Missing Payments

Choosing to downscale from certain middle-income housing options or trimming back on luxuries is an emotionally difficult decision that can feel like a step backwards – but it is considerably less painful in the long run than facing a civil judgment, having an asset repossessed, or carrying the burden of a permanently damaged credit record.

Build a Small but Consistent Emergency Buffer

Even a modest contribution of between R500 and R1 000 per month, directed consistently into a separate savings account, can make a meaningful difference over time. This kind of buffer helps absorb financial shocks – an unexpected medical bill, a car repair, a month of reduced commission – and crucially reduces the temptation or necessity to reach for more credit when those shocks occur.

| Emergency Fund Milestone | Approx. Time to Reach (at R1 000/month) | What It Can Cover |

|---|---|---|

| R5 000 | 5 months | Minor car repairs, small medical bills |

| R10 000 | 10 months | Moderate home repairs, short job gap |

| R25 000 | ~2 years | Major appliance replacement, extended illness |

| R50 000+ | ~4+ years | Retrenchment buffer of 1-2 months’ expenses |

Avoid Using New Credit as a Solution

Taking out additional loans or increasing credit limits in order to maintain a middle-class lifestyle is a strategy that NDA describes vividly – it is comparable to pouring petrol on a fire. It may appear to provide relief for a month or two, but the underlying problem is not resolved; it is amplified. The flames simply get higher.

Below are the most common forms of credit that middle-income earners typically accumulate, often without realising how quickly the combined repayments add up:

- Home loan – usually the single largest monthly commitment, often structured over 20 years

- Vehicle finance – frequently financed over 60 to 72 months, sometimes with balloon payments that create a future shock

- Credit cards – high interest rates make minimum payments a dangerous habit

- Personal loans – often taken to cover shortfalls, adding another fixed monthly debit

- Store accounts – frequently overlooked but carry some of the highest interest rates available

- Educational fees – private school fees in particular can rival a bond repayment in cost

Talk to an Expert Before It Becomes a Crisis

For those who are already in the uncomfortable position of juggling arrears, receiving collection calls or lying awake at night worrying about their financial position, the advice from NDA is straightforward – it is time to speak to a professional debt counsellor without further delay.

Debt review in South Africa is a formal, legally protected process governed by the National Credit Act. Once you are placed under debt review, credit providers are legally prohibited from taking legal action against you while the process is underway – giving you breathing room to restructure your obligations.

Many people delay seeking debt counselling out of embarrassment or the belief that it is only for people who have completely lost control. In reality, the earlier you engage a debt counsellor, the more options remain available to you – waiting too long can significantly limit what a counsellor can do to help.

Conclusion

The South African middle class finds itself caught in a financial trap of its own making – one built not out of recklessness, but out of ambition, rising costs and easy access to credit that quietly compounds over time. The path forward is not about shame or blame, but about honest self-assessment, disciplined lifestyle choices and seeking professional guidance before the situation spirals beyond recovery. Debt counselling is not a last resort reserved for those who have hit rock bottom; it is a practical, legally protected tool that works best when used early. For a generation that worked hard to reach the middle, protecting that position will require just as much effort, intention and financial awareness as getting there in the first place.

Fast, uncomplicated, and trustworthy loan comparisons

At Arcadia Finance, you can compare loan offers from multiple lenders with no obligation and free of charge. Get a clear overview of your options and choose the best deal for you.

Fill out our form today to easily compare interest rates from 19 banks and find the right loan for you.