Money on your Card in Just 3 Minutes

Fast, fair, and fee-free! Discover how Arcadia Finance can help you secure a small loan in minutes.

Arcadia Finance helps you in the search of loans from different banks and lenders. Fill in a free application and get loan offers from up to 19 lenders. We work with well-known, trusted, and NCR-licensed lenders in South Africa.

What are Small Loans?

Small loans are a widely used financial solution in South Africa, providing quick access to funds for individuals and small businesses facing immediate financial needs. Typically ranging from a few hundred to a few thousand rand, these loans are well-suited for covering unexpected expenses or managing short-term cash flow. They are designed for convenience, often featuring faster approval times compared to traditional loans, making them a practical option for addressing everyday financial challenges.

Types of Small Loans Available in South Africa

Personal Loans

Personal loans are flexible financial products that can be used for various purposes, including home repairs, medical expenses, or debt consolidation. They are available in both short-term and long-term options. Short-term loans typically feature higher monthly payments but lower overall interest, while long-term loans offer smaller payments spread out over time, resulting in higher total interest paid.

There are two primary types of personal loans: secured and unsecured. Secured loans require collateral, such as a car or property, which usually leads to lower interest rates. Unsecured loans, on the other hand, do not require collateral but carry higher interest rates due to the increased risk for lenders. The amounts for personal loans can range from a few thousand to tens of thousands of rand, making them suitable for both small and large financial needs.

Micro Loans

Micro loans are small, unsecured loans generally ranging from R500 to R2,000, aimed at individuals needing funds for everyday expenses who might not qualify for larger loans. They offer longer repayment terms than payday loans—usually spanning a few weeks to several months—providing more flexibility for borrowers.

These loans are ideal for covering household expenses or small purchases. Micro loans often have fewer eligibility requirements, making them accessible to those with lower incomes or less stable employment. However, borrowers should be mindful of the relatively high interest rates and ensure they can manage repayments comfortably.

Payday Loans

Payday loans provide immediate cash for urgent financial needs, with amounts typically ranging from R500 to a few thousand rand, requiring repayment within 30 days. While they offer quick access to funds, payday loans come with high interest rates, making them an expensive option if not repaid on time.

These loans can be beneficial for emergencies, such as car repairs or medical bills, but the short repayment term can pose challenges for some borrowers. Failure to repay promptly may lead to additional fees, increasing the risk of falling into a cycle of debt. Therefore, payday loans should be approached with caution.

Business Loans for SMEs

Business loans support small and medium-sized enterprises (SMEs) in achieving growth, expansion, or covering operational costs. Entrepreneurs can obtain funding through private lenders or government programs such as the Small Enterprise Finance Agency (SEFA) and the National Empowerment Fund (NEF), which aim to promote small business development in South Africa.

Loan amounts and terms vary based on the business’s size, financial health, and specific needs, such as purchasing equipment or hiring staff. Business loans typically have longer repayment periods than personal loans, with interest rates influenced by factors like loan size, duration, and collateral. A well-prepared business plan and financial projections are crucial for securing funding.

Eligibility Criteria for Small Loans

Before applying for a small loan in South Africa, it’s essential to meet specific eligibility criteria. Lenders typically evaluate your ability to repay the loan based on several key factors.

Basic Requirements

To qualify for a small loan, you must fulfill the following basic eligibility criteria:

Minimum Age: Most lenders require applicants to be at least 18 years old. Some may have a minimum age of 21, depending on their terms.

South African Citizenship or Residency: You must provide proof of being a South African citizen or a legal resident. Valid identification, such as an ID card or passport, will be required during the application process.

Check your eligibility for FREE!

Income and Employment

Lenders also assess your income and employment status to ensure you can repay the loan:

- Income Proof: You will need to provide evidence of income, such as recent payslips or bank statements. This documentation shows the lender that you have a steady income stream to cover loan repayments.

- Regular Employment: Being regularly employed enhances your loan application. Most lenders prefer applicants with full-time jobs or a consistent source of income.

- Self-Employed Applicants: If you’re self-employed, you can still qualify for a small loan. However, you will need to provide additional documentation, such as business financial records or proof of regular income deposits.

Credit History

Your credit score is a significant factor in determining your eligibility for a small loan:

Lenders will review your credit history to gauge your reliability in repaying loans. A good credit score improves your chances of approval and may enable you to access better interest rates.

If your credit score is low, you still have alternatives. Some lenders specialize in offering loans to individuals with poor credit, but these loans may come with higher interest rates or stricter terms. In certain cases, providing a guarantor or collateral can enhance your chances of approval.

Apply for a loan in minutes and get matched with real offers right away—find the best option for you!

How to Apply for a Small Loan

Online Application Process

Applying for a small loan online is fast and convenient. Here’s how it works:

- Choose a Lender

Research reputable South African lenders, such as Wonga, Capitec, or African Bank, that offer secure online platforms.

- Fill Out the Application

Provide personal information, including your identity and employment status, through an online form.

- Submit Documents

Upload the required documents, including your ID, proof of income, and bank statements.

- Wait for Approval

Online applications are usually processed quickly, often within hours.

- Receive Funds

If approved, funds are typically deposited into your account within 24 to 48 hours.

Why Use Arcadia Finance?

- 100% free: The application is free and does not include any hidden fees.

- Quick & easy: The whole application process is done online in minutes.

- Convenient: Compare up to 19 banks & lenders with one application.

- Non-binding: You decide if you want to accept or decline your offers.

- Safe: Your personal data is safe with us.

What is Arcadia Finance?

Arcadia Finance helps South Africans in the search for loans from different banks and lenders through our loan broker partners. We provide access to up to 19 reputable banks and lenders. By completing our loan application you will get multiple loan offers, which you can compare and select the most suitable offer. The service we offer is completely free of charge and you will not commit to anything by requesting loan offers via Arcadia Finance. We only work with trusted loan brokers who collaborate with NCR licensed banks and lenders in South Africa.

In-Branch Applications

If you prefer in-person service, many South African banks offer small loan services at their branches:

- Visit a Branch: Banks like FNB, Standard Bank, and Nedbank provide small loan assistance at local branches.

- Complete the Application: A loan officer will guide you through the form, requiring personal and financial information.

- Submit Documents: Provide physical copies of your ID, bank statements, and proof of income.

- Approval and Disbursement: Once processed, loan funds are usually transferred within a few days.

Documents Required

Regardless of the application method, you’ll need the following documents:

- Identity Document: A valid South African ID or passport.

- Proof of Income: Recent payslips or similar proof of earnings.

- Bank Statements: Three months’ bank statements to confirm income and financial status.

Compare Loans in 3 Easy Steps

Fill in our application

Complete our loan application in minutes. Just enter your details and choose your desired loan amount.

Choose a loan offer

Based on your responses, you will receive a variety of personalised offers from up to 19 lenders.

Get your money

You are free to accept or decline the offers as you please. The offers are non-binding.

How to Choose the Right Small Loan for Your Needs

Loan Amount vs Repayment Ability

When selecting a small loan, only borrow what you can comfortably repay to avoid financial strain. Larger loan amounts result in higher monthly payments, so assess your income and expenses to establish a manageable repayment plan. Avoid over-borrowing, as it can lead to missed payments and additional fees.

Loan Duration

Short-term loans have higher monthly payments but lower overall interest, while long-term loans offer smaller payments but accumulate more interest. Consider your budget when choosing between the two. If you can manage higher payments, a short-term loan may save you money in the long run.

Interest Rates and Hidden Costs

Compare interest rates from various lenders to find the most affordable option, but be mindful of hidden costs such as fees and penalties. Ensure you understand the total cost of the loan, including interest, before making a commitment.

Lenders

Always select a licensed and registered lender with the National Credit Regulator (NCR). Reputable lenders will clearly outline all terms and fees. Exercise caution with lenders promising “guaranteed approval” without proper assessment, as this may indicate a scam.

Alternatives to Small Loans

Borrowing from Family or Friends

One common alternative to small loans is borrowing from family or friends. This informal lending arrangement can be beneficial as it typically doesn’t involve interest rates or strict repayment schedules. However, it’s crucial to manage these situations carefully to avoid straining relationships. Establishing clear terms for repayment, even informally, can help maintain trust and prevent misunderstandings. This option can often be quicker and less stressful than applying for a loan through formal financial institutions.

Savings and Emergency Funds

If you have savings or an emergency fund, this can be a great alternative to taking on debt. Using your own money to cover unexpected expenses means you won’t have to worry about repaying a loan or accumulating interest. Building a savings buffer is a solid long-term strategy for financial security. Even setting aside a small amount each month can help you avoid borrowing in the future when financial emergencies arise.

Credit Cards

For those with access to a credit card, this can sometimes be a better option than taking out a small loan. Credit cards often come with more flexible repayment terms, and if managed responsibly, you can avoid paying interest by repaying the balance in full each month. However, credit cards can carry high interest rates if you carry a balance over time, so they should be used carefully. It’s worth comparing the costs of using a credit card versus taking out a small loan, especially for short-term needs.

Government Assistance Programs

In South Africa, various government assistance programs are designed to help low-income individuals and families. These programs offer financial support in the form of grants or low-interest loans, providing a safer alternative to high-interest small loans. For example, the South African Social Security Agency (SASSA) provides grants that can assist those facing financial hardship. It’s worth exploring these options before turning to private lenders, particularly if you qualify for government aid that doesn’t require repayment.

Secure your loan effortlessly with Arcadia Finance

The loan application is free, and you can pick from a variety of 19 respected lenders. We only work with trusted loan brokers who collaborate with NCR licensed banks and lenders in South Africa.

After submitting your loan application to us, we will send it through our loan broker partners to a number of different banks and lenders for review. Within minutes, you’ll receive a variety of loan options that are available for you. Select the one that best fits your needs.

Remember, all offers are no-binding, so if you don’t find what you’re looking for, you’re free to decline.

Conclusion

Small loans can serve as an effective financial solution for short-term needs in South Africa, allowing individuals and small businesses to access funds quickly. However, it’s important to understand the different types of loans available, including personal loans, payday loans, and micro loans, as well as their associated costs and repayment terms. By comparing various lenders and considering alternatives such as borrowing from family, utilising savings, or exploring government assistance, you can make informed and prudent financial decisions. Always remember to borrow only what you can comfortably repay to prevent unnecessary financial pressure.

Frequently Asked Questions

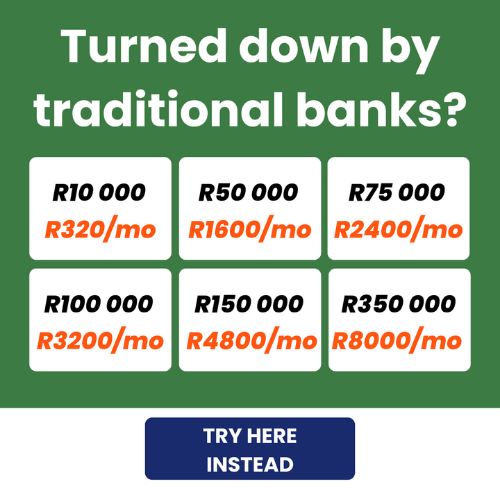

A small loan is a short-term financial solution, typically ranging from R500 to R50 000 (approximately $26.30 to $2 893.80), designed to cover urgent or everyday expenses. These loans usually have faster approval times compared to larger loans and are available from various lenders in South Africa.

To qualify for a small loan in South Africa, you must meet basic requirements such as being over 18 years old, providing proof of South African citizenship or legal residency, and demonstrating a steady income. Lenders will also evaluate your credit history and ability to repay the loan.

There are several types of small loans, including personal loans, payday loans, and micro loans. Each type has different terms and repayment conditions, allowing borrowers to choose based on their specific financial needs and repayment capabilities.

Interest rates on small loans vary depending on the type of loan, the lender, and your creditworthiness. Payday loans typically have higher interest rates due to their short repayment periods, while personal loans may offer lower rates if secured by collateral or if you have a good credit score.

Yes, alternatives include borrowing from family or friends, using your savings or emergency funds, or exploring government assistance programs such as grants for low-income individuals. These options may help avoid the interest and fees associated with small loans.